Industrial availability across South Florida has risen to its highest level on record, but recent trends suggest the region’s three largest markets are no longer moving in lockstep.

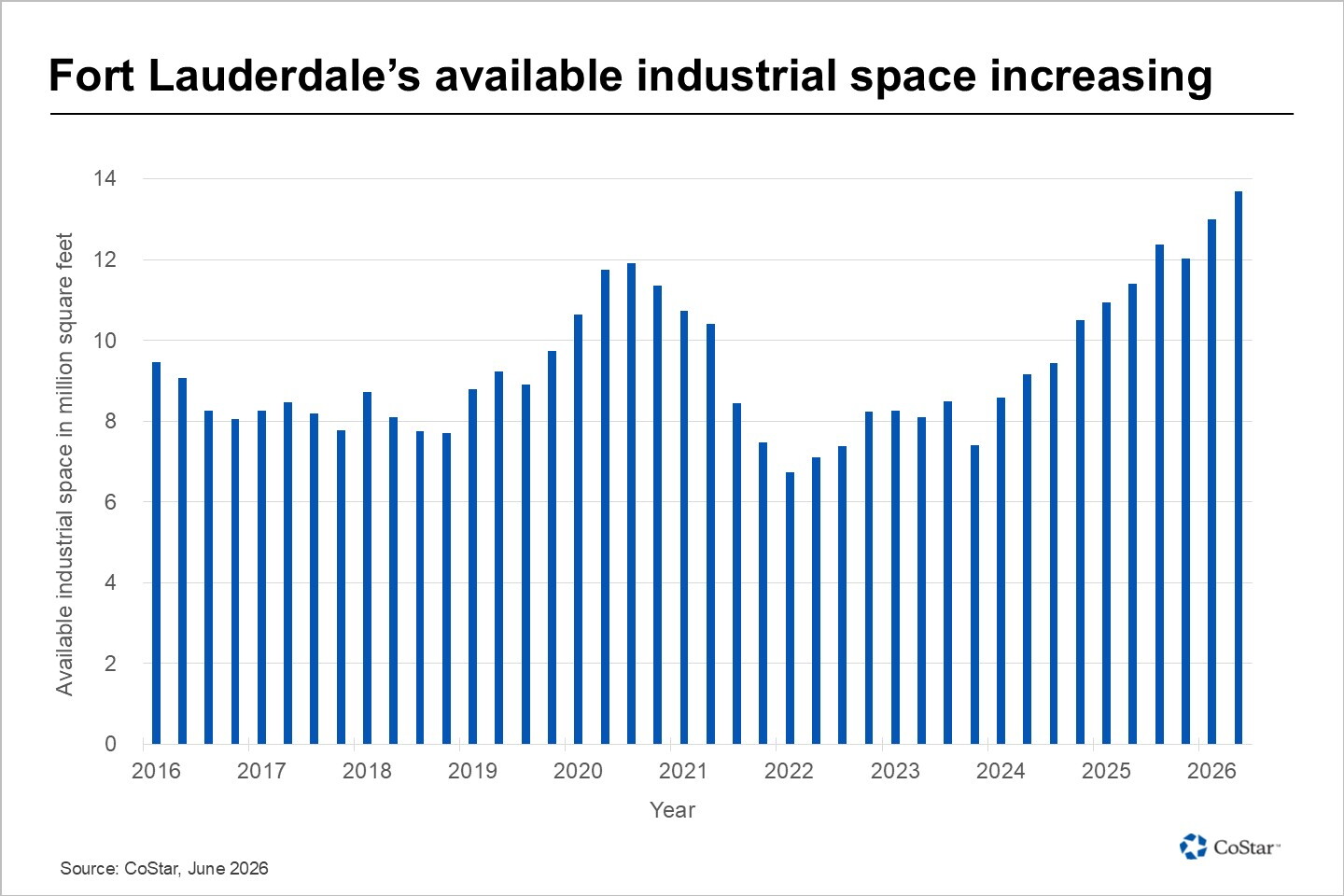

While availability continues to increase in Fort Lauderdale, both Miami and Palm Beach are beginning to show signs of stabilization after several years of rapid expansion.

Availability rates remain elevated across all three markets. In Miami, availability stands at 6.6%, nearly double the 3.6% recorded in the second quarter of 2022, while Fort Lauderdale has climbed to 9.4% and Palm Beach to 8.7%, according to CoStar data. All three markets have seen availability rise sharply from pandemic-era lows, reflecting a wave of new construction that has added tens of millions of square feet of industrial space since 2020.

That supply growth has played out unevenly across the region. Miami, the largest market with more than 280 million square feet of inventory, has delivered over 27 million square feet since 2020, helping push availability to record levels. However, the pace of increase has slowed more recently, suggesting the market may be nearing a turning point. Palm Beach, by contrast, has followed a steadier trajectory. With a smaller inventory base of roughly 71 million square feet and a more modest development pipeline, the market appears to have flattened earlier, with availability levels slowly increasing after rising sharply through 2022 and early 2023.

Fort Lauderdale stands apart as the only market where availability continues to rise without clear signs of leveling off. The market’s availability rate has climbed to its highest level in the data series, supported by ongoing deliveries and an active development pipeline. While smaller than Miami, Fort Lauderdale’s inventory of nearly 144 million square feet has expanded significantly in recent years, and the market is still working through that new supply.

Demand trends help explain the divergence in performance. All three markets have recorded negative net absorption over the past year, indicating that more space has been vacated than leased. However, conditions are improving in some areas. Miami’s net absorption, while still negative, has rebounded from deeper declines in 2025, while Palm Beach has experienced a comparatively smaller pullback. Fort Lauderdale, on the other hand, continues to post weaker demand metrics, contributing to its rising availability.

The imbalance between supply and demand has also weighed on rent growth. Annual rent increases have slowed sharply across the region, falling to 1.3% in Miami and 0.9% in Fort Lauderdale, down from double-digit gains just two years ago. Palm Beach has maintained slightly stronger growth at 2.1%, reflecting its more stable availability trend and comparatively limited pipeline.

Looking ahead, the trajectory of each market will likely depend on how quickly demand can absorb the recent wave of new construction. While signs of stabilization are emerging in Miami and Palm Beach, Fort Lauderdale appears earlier in that adjustment process, with elevated availability likely to persist until new supply is more fully leased.